The Evolution and Future of PV Manufacturing - Insights from Radovan Kopecek at IEEE-PVSC

Dr. Radovan Kopecek’s IEEE-PVSC keynote traced the evolution of crystalline silicon solar technology and the barriers overcome along the way, from PERC to TOPCon and back contact. Backed by over 7 GW of global tech transfer projects, his perspective offers a front-line view of PV manufacturing trends and the policies shaping them.

· Malcolm Abbott · 8 min read

The keynote at this year’s IEEE-PVSC was delivered by Dr Radovan Kopecek of ISC Konstanz, offering a front-line view of global PV manufacturing. His talk explored how regional policies and market forces are shaping technology choices, the barriers that must be overcome, and the industry’s relentless progression from PERC to TOPCon and now toward back contact technologies.

Rado is one of the busiest, most visible people in the PV technology world. If you go to a conference he will almost certainly be there. For over 30 years he has brought passion and energy to his work and is a tireless advocate for crystalline silicon and solar energy more broadly. Like everyone in this business, he has a particular perspective and a particular opinion. In this blog post I attempt to summarise Rado’s perspective as he presented it in his talk.

With permission from Dr Radovan Kopecek, we have summarised some key points from his talk and included some of his slides in this article.

A Front-Line View from ISC Konstanz

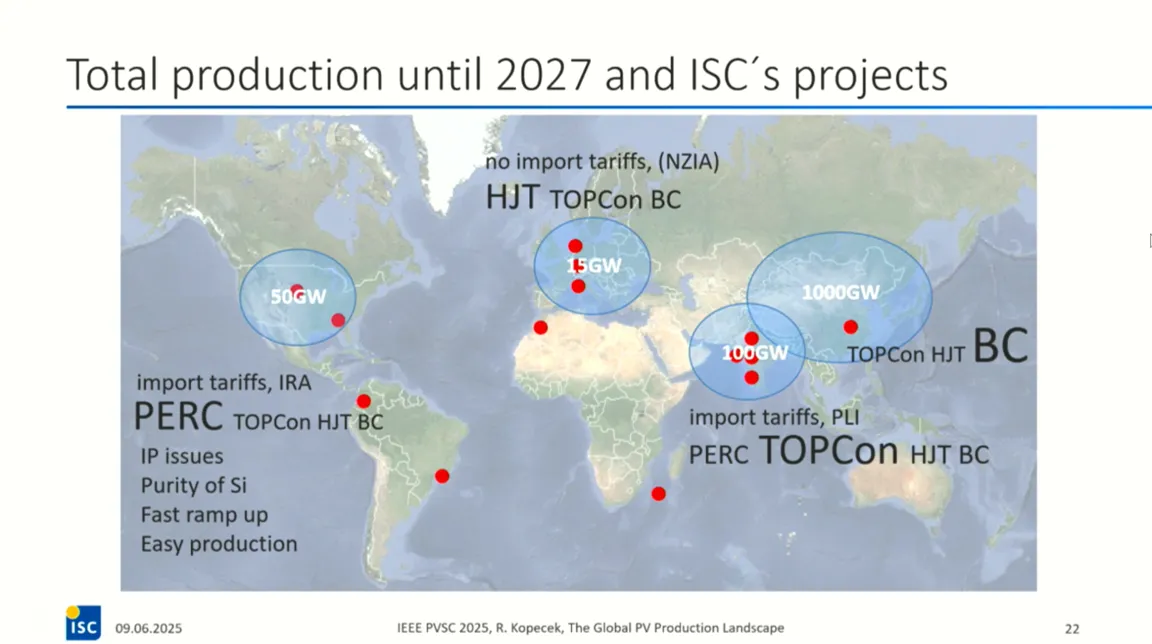

Why specifically is Rado an interesting person to get perspective on this topic? It starts with how ISC Konstanz (which he co-founded and is a director of) have positioned themselves as a bridge between academia and industry. From the outset, they championed n-type and bifacial technology and have continued to prioritise turning these innovations into practical, commercial solutions. Building on this, they have developed a highly effective technology transfer service, enabling manufacturers to adopt cutting-edge innovations at scale. Many academic institutions have attempted to succeed in this space, but in 2025 the team at ISC Konstanz has clearly established itself as a leading provider of services for setting up new factories and ramping technology. In his talk Rado specified ten tech transfer projects they had worked on which added up to over 7 GW of production capacity (see the red dots on the slide below). Interestingly they have done this into a variety of countries including China, India and the US. This all adds up to them having a front-line view of what is happening with global PV production.

Regional Strategies in PV Manufacturing

The slide shows Rado’s high-level summary of PV production in the four main regions globally (including predicted new capacity installed up to the end of 2027). The numbers are rounded off, but they give a good idea of the relative scale. China dominates with 1000 GW which is 10x the next closest India. The only other significant region is the US. Another interesting observation is the split in technology selection for new capacity in the different regions. China is in a state of over-capacity and are mostly installing back contact technology (BC) which is the most complex and advanced technology. India on the other hand seem focused on installing TOPCon. Rado did not give a specific reason for this, however it likely relates to the maturity of manufacturing process for TOPCon. Strangely the US is installing PERC cells which are a couple of steps backwards in terms of technology complexity. The reasons given for this were IP issues and the relatively lower purity of silicon. I assume that last point refers to the locally produced silicon which is using older technology.

What It Takes to Compete Locally

Rado highlighted the conditions required to make local manufacturing possible. He specified two key requirements. There must be import tariffs to protect against cheaper overseas imports, and local funding schemes that further incentivize local manufacturing. Both of those conditions exist in the US and India resulting in the growth of the local industry. In Europe, once the heart of PV manufacturing, no such protection exists and as a result production is low. The state and future of European industry was revisited several times during his talk. There are some initiatives being discussed, however it sounds like overall the focus of Europe into the future will be on R&D, manufacturing tools and supporting production in India and the US.

Falling Costs, Evolving Technologies

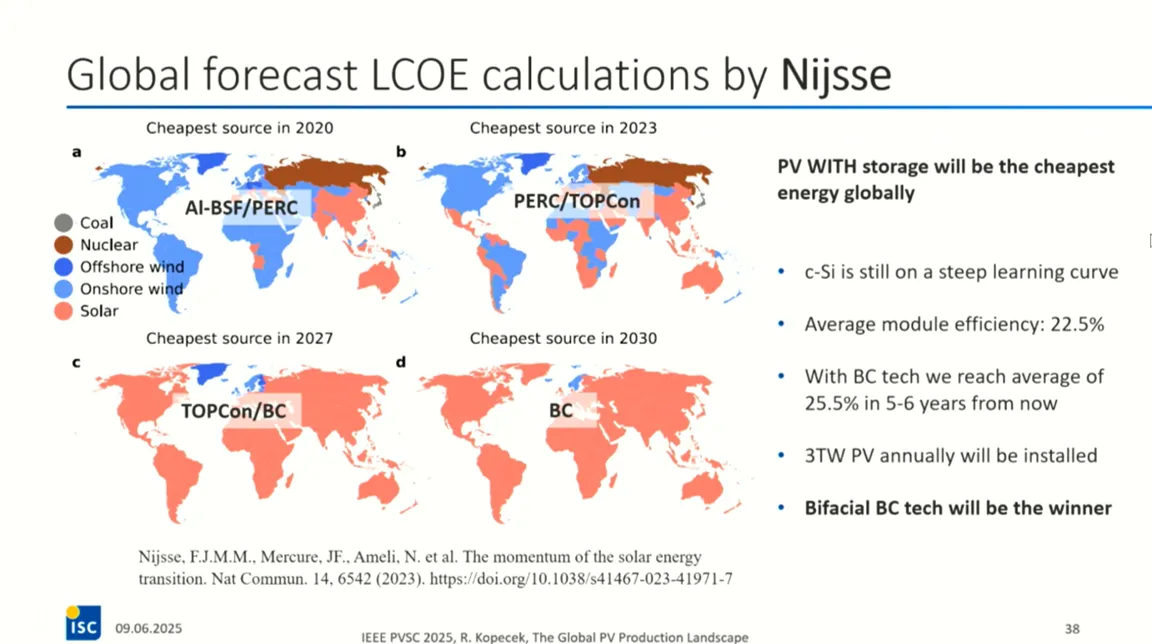

At the core of Rado’s talk was the ongoing technological progression of crystalline silicon solar cells. The continued ability of the industry to innovate, improve and then transfer new technologies all the way into final products has been one of the key factors driving down the cost of solar energy. Rado spoke at length about the growth and momentum of the solar market. There are a lot of different ways people present that information, often as bar charts or line graphs. Something new for me, although it was published a couple of years ago, is shown in the slide above. It plots the global map of which energy generating technology has, or is predicted to have, the lowest levelized cost of electricity (LCOE) in each location. To be honest, I’ve not read that paper, but I like the graph. As a member of the solar energy industry, it is pleasing to see the spread of pink (solar energy) across the globe. In his talk Rado links the continuous technological evolution to the reduction of LCOE and the spread of solar energy. He overlays the dominant production technology, and it highlights his (and others) roadmap: Al-BSF to PERC to TOPCon to back contact.

At SunSolve we’ve witnessed the same progression that Rado described. Each time the industry faced a barrier—whether it was selective emitters, PERC passivation, or the leap to TOPCon, new solutions emerged and quickly became mainstream. Our own development path has mirrored this journey, with SunSolve continually evolving to support each new generation of technology, for example, adding new contact schemes, layouts, and optical models. Like Rado, we believe the industry will continue to overcome these hurdles, with back contact cells next in line to reshape mass production.

How the Industry Leapt Each Hurdle

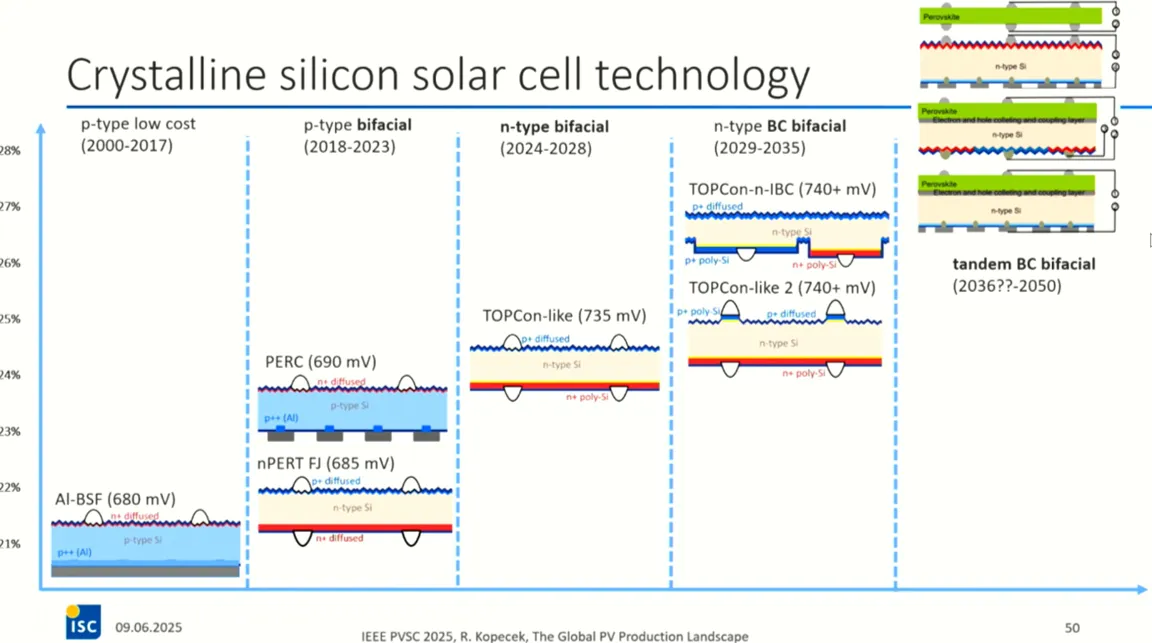

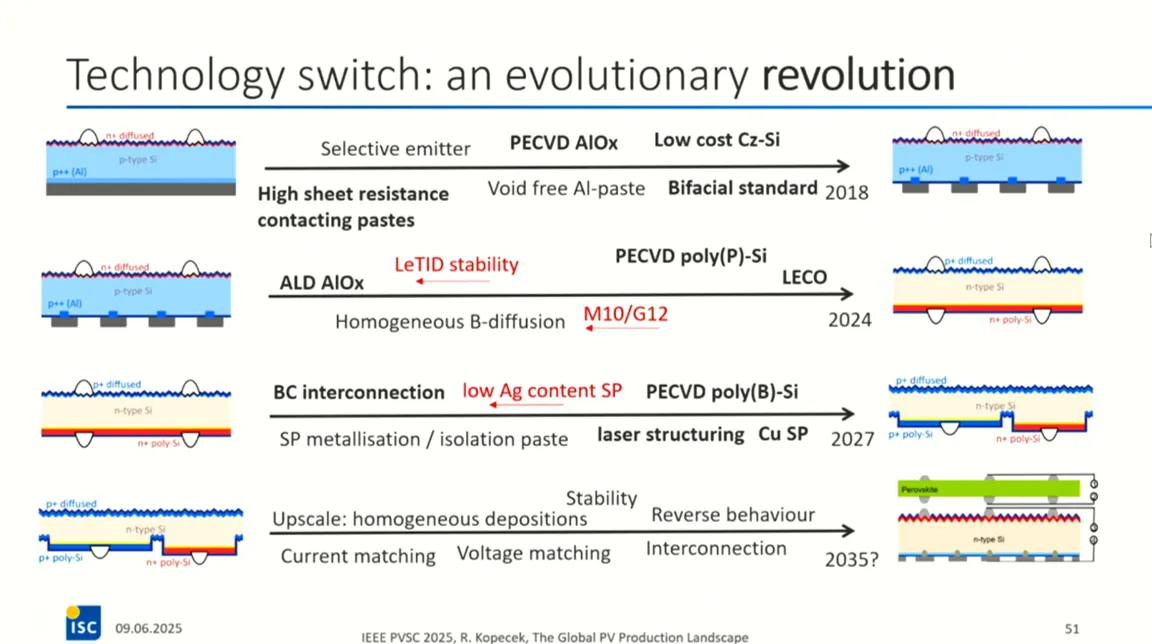

Rado further drove home the evolution of solar technology by reviewing the history of key breakthroughs that have enabled it in the past. When I first started in the solar industry the world was dominated by the Al-BSF solar cell. My PhD work and first job looked at ways to develop selective emitters that could be manufactured easily. It is pleasing to see the humble selective emitter make the list, however Rado highlights the two key technologies that truly enabled the shift to PERC. The creation of a PECVD AlOx process (to passivate the rear p-type silicon) and the innovations that resulted in very low-cost mono-crystalline silicon wafers. If you were working in the industry at the time, it often felt like PERC cell was never quite going to become a commercial reality, until suddenly it was in every manufacturing line. Similar for the TOPCon cells, the creation of LECO technology and PECVD poly-silicon has enabled the transition away from PERC. Rado is clear on this trend, the industry has a great ability to continually leap over the technological barriers and enable the next generation of improved solar cells.

Bifacial Back Contact on the Horizon

The current challenge is the transition into mass production of highly efficient all back contact (BC) solar cells. It seems a strange statement given that companies like SunPower (later Maxeon) have had commercial products in this space for many decades and others like Aiko clearly have products. Indeed, the slide shown earlier claimed that China is exclusively rolling out new BC lines. Nevertheless, challenges no doubt exist, costs can be reduced and perhaps the timing relative to old patents is also telling. Specifically, Rado highlights the need for better boron doped polysilicon, better laser structuring tool (and supporting processes) and copper screen print pastes.

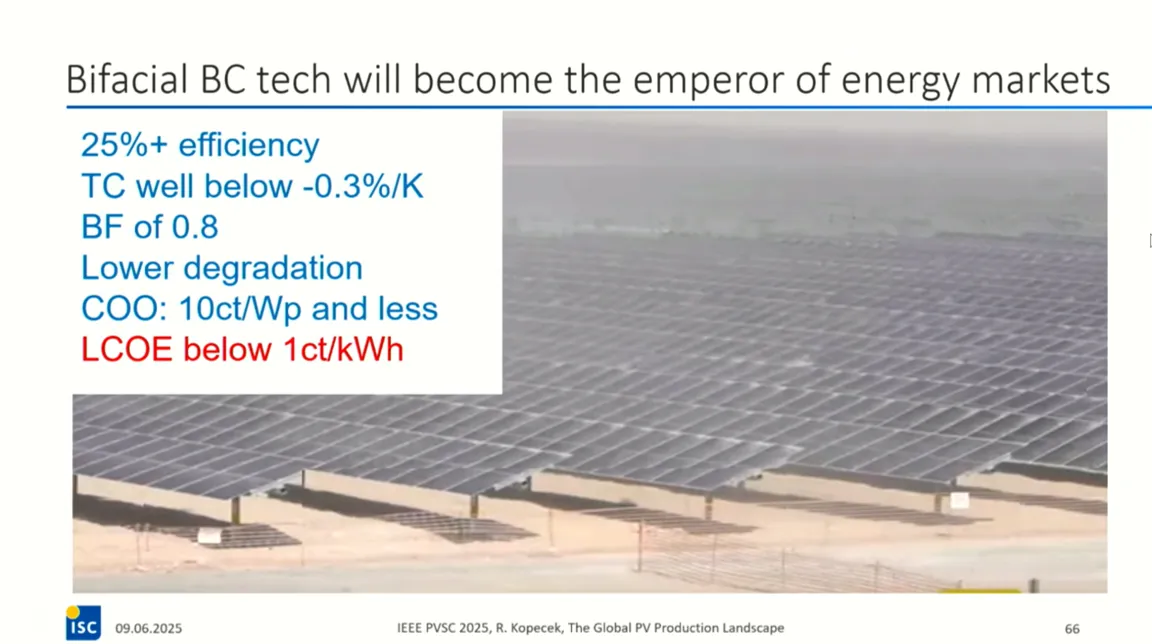

“In order that a technology becomes mainstream, it must be bifacial and must makes sense on large scale systems.”

That quote from his talk is an interesting one and it does highlight another challenge for BC technology. How to be bifacial? Despite what intuition would tell you, apparently these devices are currently 73% bifacial (this means that normally incident light striking the rear side of the panel will be converted into electricity with 73% the efficiency with which the front side would do it). That is already surprisingly good given that both metal contacts have been located onto the rear where they can shade the light. Rado expects this to improve further to 80% which he gave as a target the industry is on track to achieve.

“Bifacial back contact will be the technology that will drive the energy transition”

It is not yet confirmed that back contact technology will become the dominant cell type in mass production. However, Rado’s position on its future is clear. He believes that like previous technology hurdles, with the full focus of the industry, all barriers will be smashed and by 2027/2028 bifacial BC will dominate the market.

Our Journey Along the Same Roadmap

Here at SunSolve we love helping our customers push the boundaries of solar technology. Whether you’re tackling challenges with TOPCon, back contact, or quantifying bifacial gain in real-world conditions, you can leverage our years of experience working alongside the industry to overcome these hurdles. Reach out and we’d be happy to show how SunSolve can support your work.

Acknowledgments

Thanks to Dr. Radovan Kopecek and the team at ISC Konstanz for sharing their insights and for their decades of work advancing crystalline silicon solar technology. Their leadership in bridging academia and industry continues to shape the future of PV manufacturing worldwide.

This work was supported by funding from the Australian Renewable Energy Agency (ARENA). The views expressed herein are not necessarily the views of the Australian Government, and the Australian Government does not accept responsibility for any information or advice contained herein.